{kind=link}

A reform built on data sharing, security standards and public confidence may redefine inclusion and competition — if the system avoids fragmentation and institutional fatigue.

Lima, December 2025

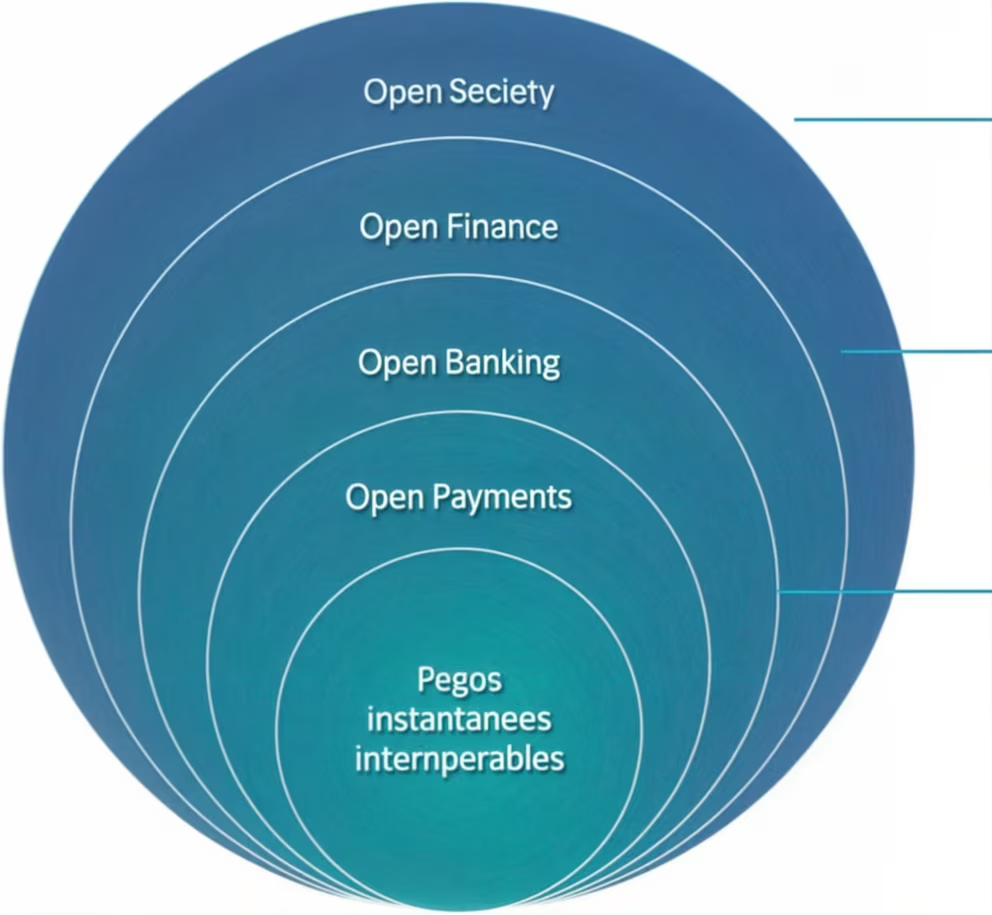

Peru is entering a decisive phase in its digital-finance evolution. With regulators preparing to release a comprehensive Payments Regulation and a national roadmap for Open Finance, the country stands on the threshold of a structural redesign that extends far beyond banking. Authorities at the Superintendencia de Banca, Seguros y AFP and the Banco Central de Reserva del Perú aim to construct a framework capable of integrating insurance, pensions, credit, payments and fintech services under a unified architecture. The ambition is national in scale, yet its success hinges on whether Peru can build an ecosystem that balances innovation with rigorous oversight.

At the center of this transition lies the technical mandate of interoperable APIs. These interfaces, when implemented with consistency and strict governance, allow financial institutions, insurers, fintech firms and authorized third parties to exchange data securely and in real time. In theory, they should enable faster onboarding, personalized credit products, micro-insurance for vulnerable populations and more agile payment flows. Specialists from European supervisory bodies note that nations that have achieved robust API ecosystems did so only after adopting strict standards for authentication, encryption and consent management, combined with a clear legislative backbone that minimized ambiguity.

Latin America offers lessons that Peru cannot afford to ignore. Brazil, frequently cited by the OECD as a regional case of rapid Open Finance maturation, shows that coordination among central banks, supervisory agencies and market actors remains the non-negotiable foundation of success. Fragmentation, in contrast, has delayed progress in several countries where regulations preceded infrastructure, or where institutions launched pilots without a cohesive national strategy. Analysts in North America emphasize that Peru has the advantage of observing both paths and choosing the disciplined one.

For Peru, the stakes are socioeconomic as much as technological. Nearly half of the adult population remains underserved or excluded from formal financial services, according to regional development estimates. Open Finance could alter this landscape by enabling tailored credit scoring, access to microloans for individuals lacking traditional banking history and the expansion of secure digital wallets in rural and peri-urban areas. Development economists from multilateral institutions argue that if implemented correctly, the reform may accelerate financial inclusion at a scale comparable to the expansion of mobile payments in Africa, but only if trust and usability align with infrastructure deployment.

Trust, however, is the most fragile variable. Public confidence depends on whether citizens feel that data sharing enhances their autonomy rather than exposes them to vulnerabilities. The challenge extends beyond technology: it includes literacy, transparency and cultural adaptation. Behavioral researchers in Europe highlight that individuals will consent to data sharing only when they understand its purpose, perceive clear benefits and believe that institutions can safeguard their information. A misstep in the early stages — such as a privacy breach, an unclear consent mechanism or inconsistent communication — could undermine adoption for years.

Institutional capacity also forms a critical pillar. Banks and fintech companies must deploy security layers that meet international standards, and regulators must strengthen monitoring teams trained in cybersecurity, digital-risk assessment and behavioral fraud analysis. Experts from Asia caution that Open Finance systems fail not because of weak conceptual design but because of insufficient enforcement capabilities once real-time data flows increase. The volume of transactions, combined with the sophistication of cyber threats, requires a regulatory posture that is proactive rather than reactive.

In practical terms, the new ecosystem will reshape competition. Fintech firms will benefit from the ability to integrate directly with banks and insurers, offering consumers more agile services. For traditional institutions, the shift will demand cultural transformation. They must transition from closed data silos to a model in which collaboration, transparency and innovation form part of daily operations. Industry leaders across the Pacific region warn that incumbents that resist this shift risk losing relevance in markets increasingly driven by user experience and digital agility.

The geographic dimension further complicates implementation. Peru’s economic distribution reflects disparities between Lima and other regions, and Open Finance must be designed to function effectively in areas with limited connectivity. Infrastructure gaps may undermine real-time interoperability unless addressed in parallel with regulatory reform. This means national strategies must include investment incentives for digital infrastructure, partnerships with telecommunications providers and targeted programs for remote areas to ensure equitable adoption.

Across the private sector, anticipation is high. Fintech companies envision a surge in innovative products: dynamic credit lines that adjust to income cycles, micro-insurance tailored to informal workers, integrated savings platforms for small merchants and high-speed settlement rails for domestic and cross-border payments. Yet, their success will depend on building trust with consumers who may be wary of sharing personal data in an environment still learning to distinguish between innovation and risk.

As Peru moves toward operationalizing Open Finance, the country faces a crossroads: either build a secure, cohesive and inclusive system that elevates its financial infrastructure to global standards, or risk constructing an ecosystem fragmented by inconsistent implementation. The months ahead will determine whether the regulatory milestones translate into a durable transformation or remain a well-intentioned blueprint. The opportunity is historic, but so is the margin for error.

Phoenix24: the visible and the hidden, in context. / Lo visible y lo oculto, en contexto.